Dividend Growth Stocks Discussion and Rankings

"You won't believe who's number one!"

TL;DR

Though it does present some advantages, exclusively investing in stocks that pay a dividend likely has a high opportunity cost. However, for someone who can afford to pay the opportunity cost, dividends are a compelling way to make passive income. Dividend growth stocks make the most sense to a young/not-yet-retired investor if they are planning to borrow to invest.

After screening for dividend stocks with a yield over 1%, a history of dividend growth and a payout ratio of less than 80%, I scored the candidates based on relative rankings of dividend yield and dividend growth. The results are below.

Top 10 Dividend Growth Stocks in Canada at time of writing:

The full list and criteria are later in the article, after a more in-depth discussion of the costs and benefits of stocks that grow their dividend – dividend growth stocks.

None of this is definitive in any way, I’m just a DIY Guy (teacher by day), so do your own research and get professional financial advice.

Introduction:

Despite typically writing about high-growth microcaps, smallcaps, and compounders, my attention recently turned to dividend growth stocks (stocks that consistently grow their dividend over time).

This is because, firstly, opportunities where I’ve been hunting are drying up quickly, and quality dividend growers help balance an aggressive portfolio in the short-term, and in the long-term can provide attractive income when I work less or fully retire.

Keystone Financials’ “StockTalk” podcast discussed this the other day, and I thought it was a useful discussion:

. This is the gist:

Essentially, snowball your savings with smallcaps and retire with dividends. I’ve got a good start on the smallcap snowball, so devoted some time to the dividend retirement idea. This post is the result.

Costs and Benefits of Dividends

Cost #1 – Opportunity Cost

If you don’t immediately need additional income, and there’s a company that internally generates high returns but doesn’t pay a dividend, I don’t think it should be overlooked; if a company can compound, take advantage.

Take for example the dividend investor who didn’t buy FAANG stocks in the 2010s because many didn’t pay dividends; they missed out on life-changing returns. Now that some do pay a dividend (eg Google), dividend investors are buying them after the best part of the run is over and the next market leaders are elsewhere. Dividend hunting for the sake of it can induce a bad case of skating to where the puck was, not where it’s going.

On the other hand, investors who avoid dividend stocks just because they pay a dividend are making the same mistake, just inverse. Plenty of great compounders pay dividends; we shouldn’t discount a stock’s ability to compound by whether it pays a dividend. In a phrase, dividends are frequently irrelevant to total returns.

This is the main problem with dividend exclusive investing and, to me, overwhelms most of the immediate benefits (as a young person). The opportunity cost of dividends, if we could weight this post by significance, would be 95% of it.

Benefit #1 – Psychological Edge

I said dividends were irrelevant to total returns, but that was only on paper. In the real-world dividends provide a psychological advantage that may make a difference. Getting cash in the mail for doing nothing is like heroin to the veins.

As the truism goes, “Time in the market beats timing the market,” so anything that keeps an investor invested is probably worth it. Stock prices go up and down, tempting many to sell prematurely. If that means sacrificing theoretically better total returns to pay a dividend that keeps the investor invested during the good times and bad, then definitely own dividend paying stocks.

Owning stuff that goes up over time is the entire game and if dividends provide the psychological edge that keep an investor invested, then dividends are good. I don’t think it applies strongly to me, but I do eagerly open emails saying I’ve received “free” (not actually) money.

Cost #2 - “Dividend Retirement” Requires a lot of Money

5% of $1,000,000 (a lot of money) is $50,000 a year (not a ton).

A million dollars is rather hard to get for most people and a fifty-thousand-dollar income (before taxes) would require many people to be quite thrifty, particularly if they have housing costs like a mortgage or rent. This is why I’m personally leaning towards investing for total return when young and prioritizing dividends when (or if) I can afford to.

Investors who were buying exclusively dividend growth stocks for the last twenty years with the goal to retire on the dividends, would probably have higher dividend income if they’d been buying Constellation Software and Berkshire-Hathaway during that time instead, and then put the much higher absolute amount into dividend stocks now.

The returns are obviously better for Constellation, although Royal Bank tripling in ten years is not bad at all either. What’s the trade-off for the hopeful dividend retiree?

I know I’ve cherry-picked my example here to make a point, but I felt it worth noting that even an investor hoping to retire on dividends may want to forgo them in favour of stocks that accelerate accumulation, for the time being.

Benefit #2 – A Dividend Retirement vs “The 4% Rule”

If you can manage to get enough of a nest egg to fund retirement with mainly dividends then there are real advantages over the more traditional retirement strategy of funding your retirement by selling 4% of your assets per year.

Not having to sell anything and still having enough income is significant. One of the biggest risks to a retirement reliant on selling is if the assets suddenly drop in price, especially at the start. Then the retiree must sell them for cheap to buy food today, leaving less for the future; I’ve learned this is called “sequence risk,” and can materially shorten the duration of one’s savings. If you get a 4% yield from your investments however, you may not have to sell the dip, or are required to sell less, reducing sequence risk.

Dividends in retirement also reduce the need for sophistication. Knowing what to sell and when takes skill and probably professional services, which come with fees. Just sitting around and letting 4-6% roll in without requiring thinking or looking at stock prices is a behavioural advantage.

As long as the dividend retiree doesn’t completely ignore total return in favour of full dividend orthodoxy (the opportunity cost could be steep), I expect having yield reduces sequence and behavioural risk in retirement, a good thing.

Cost #3 – Taxes

Another reason I don’t love dividends as a young person, is that they will frequently add to my taxable income (unless the stock is in a registered account). Instead of making X dollars, I’ll make $X + dividends. Put another way, if I’m getting a 4% yield on my dividend stocks, after taxes it’ll likely be closer to 3% because they count as income and will be taxed too.

If I can shield investment gains from taxes before I need the cash (by having companies keep and reinvest the cash entitled to me rather than paying it out), then I’m in favour of that – let the Boomers pay for their own diabetes monitors.

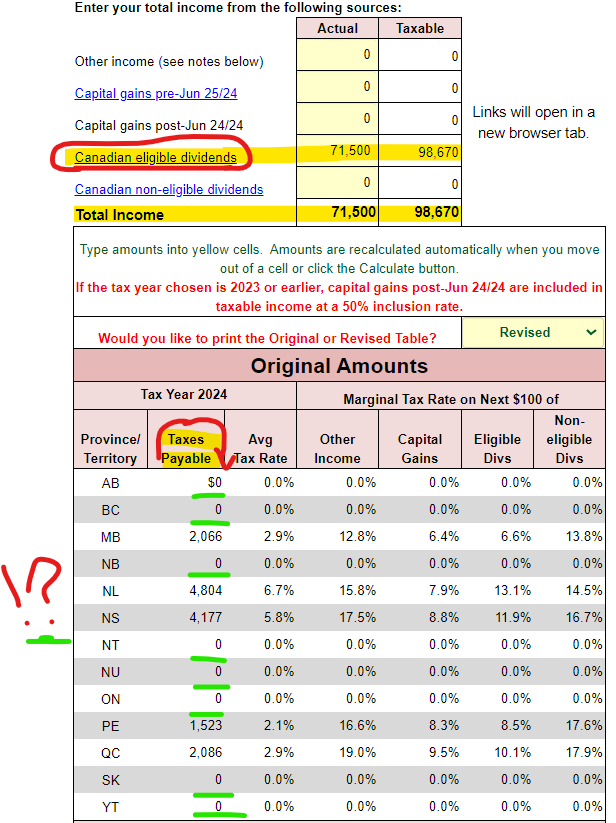

Benefit #3 – Canadian Taxes

If you don’t have a job though, dividend income in Canada is incredibly tax efficient. If an individual makes nothing but Canadian dividend income in a year, the first $71,500 is TAX-FREE in most provinces, and only a bit more in others:

Imagine paying no taxes. It’s almost unbelievable, especially when you consider many people retire as couples and can take advantage of this twice-over.

To illustrate how amazing this is, if I were to make $71,500 from a job or GICs or bonds, instead of paying $0 in tax, I’d pay around $15,000:

Taxes reduce a typical $71,500 income to around $56,500, or around $1,250 a month – that’s quite a bit. In short, with dividends you keep more of your money at tax time, sometimes all of it, meaning you need less of it to retire. Capital gains income makes it more complicated, but dividends are, at the very least, a very tax-efficient way to support retirement in Canada. Who knows if it will stay that way, but for now it remains compelling.

Benefit #4 – Dividends Grow, Interest Payments Don’t Necessarily

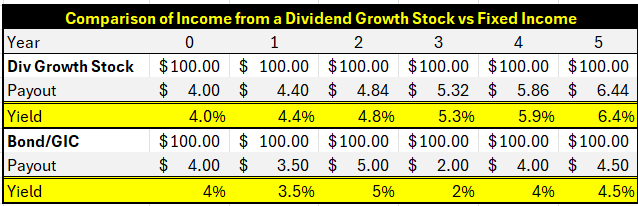

A good dividend growth stock can grow dividends annually by 10% or more for decades. This is significant, firstly, because it means your income grows with or more than inflation. That is NOT true for bonds or fixed income.

For example, someone buys a $100 dollar dividend growth stock with a 4% yield so receives $4 that year. Their friend buys a $100 one-year bond with the same yield so receives $4 in interest. Ignoring taxes (dividends get treated better), these are functionally the same investment income-wise, both the person and their friend are receiving $4.00 – until the next year rolls around.

Next year, the dividend growth stock raises its dividend by 10%, from $4/share to $4.40/share. Recall the investor paid $100 for the stock so their new yield is 4.4% ($4.40 / $100). The friend’s bond matures so must reinvest in a new bond. The new yield will be determined by prevailing interest rates, which could be higher or lower than the previous year (known as “Roll-over Risk”). Rates at 3.5% means the friend is getting paid only $3.50 ($3.50 / $100) instead of the prior year’s $4.00, while higher rates of say 5% would mean they’ll receive $5.00 ($5 / $100).

This is purely illustrative but notice how fixed income’s yield can jump around (with interest rates), while a solid dividend growth stock (growing its dividend at 10% a year) will see its yield continually rise.

Here it is visually:

The bondholder/fixed income investor’s yield is reliant on interest rates, while the dividend growth investor, provided they’ve chosen a quality company or companies, will see their yield rise over time.

In extreme circumstances, certain companies will raise their dividend so aggressively and for such a long time that long-term investors are receiving huge yields. Warren Buffet, for example, was an early investor in Coca-Cola. Legend has it that when Coke began paying a dividend, he received dividends as large as the sum he initially paid for the stock, for a yield of 100%. This is a tantalizing possibility.

The risk is that equities can go down and dividends can get cut while bondholders almost always get paid. I’m not in a position where that matters to me yet, but I’ll weigh those risks when I get there. For now, I’m just exploring ideas.

Uncategorized Thought – Are Dividend Stocks Ideal Candidates for Leverage?

In Canada, if you take out a loan to invest in income-producing assets, like rental properties or dividend stocks, the interest you pay on the loan is tax-deductible, meaning you can use that interest expense to lower your taxable income, resulting in less taxes paid (in the same way as RRSP contributions). Between the tax refund and cash dividends, your interest on the loan is likely paid, and you get to keep the compounding.

There are risks with this idea of course, there always is with debt, but they are little different to someone borrowing to buy a rental/investment property: if you can’t pay, you lose the asset, whether it’s equity in a house or a company. The main difference between an investment property and borrowing to buy dividend stocks is that instead of a tenant “paying the mortgage,” reliable companies like Fortis, Telus, and Royal Bank are.

There are smaller differences, like being able to diversify in stocks versus real estate, not needing as much leverage to get similar returns, and improved liquidity (being able to buy and sell faster and cheaper). The main point, however, is that borrowing to buy dividend growth stocks may be more unpopular than it is risky.

The Smith Manoeuvre is something to look more into if this is appealing and applicable.

Dividend Stock Rankings - Finally

Because of these thoughts I took a close look at what dividend growth stocks are out there. Here’s how I did it and what the results were.

Methodology:

Firstly, I screened for Canadian dividend paying stocks that have a history of growing their dividend and a payout ratio of less than ~80%. I curated the list a bit by removing certain companies that screened well enough but had other issues, like worrisome-looking debt, clearly superior peers I’d rather own (eg certain banks and insurers), are in a tough business (eg oil field services), are in a declining business (eg phonebooks), and/or businesses whose numbers are frequently misleading (eg certain financial services companies). I was liberal with the cuts and didn’t look very hard for good ones that don’t screen well, so if your favourite isn’t on the list, just let me know and I’ll include it if it fits.

Having arrived at a rough list of prospects, next I assumed the most important factors to a dividend growth investor are dividend yield (what percent of the stock price comes back to the owner in a cash dividend each year), and recent dividend growth (by how much that cash payment grows each year). This is because dividend growth investors primarily want income (yield) that increases over time (growth).

To score our prospects, I ranked them against each other across those two metrics: dividend yield and dividend growth. For example, the highest yielding stock of the 45 got 45 points in the yield category, while the lowest yielding stock got 1-point, average-yielding stocks got middling scores around 22, and the others filled in the rest. I repeated that process for dividend growth, ranking them from best to worst and assigning points based on where they placed in that order. For each company, I added up the points received in both categories to arrive at a score.

Results

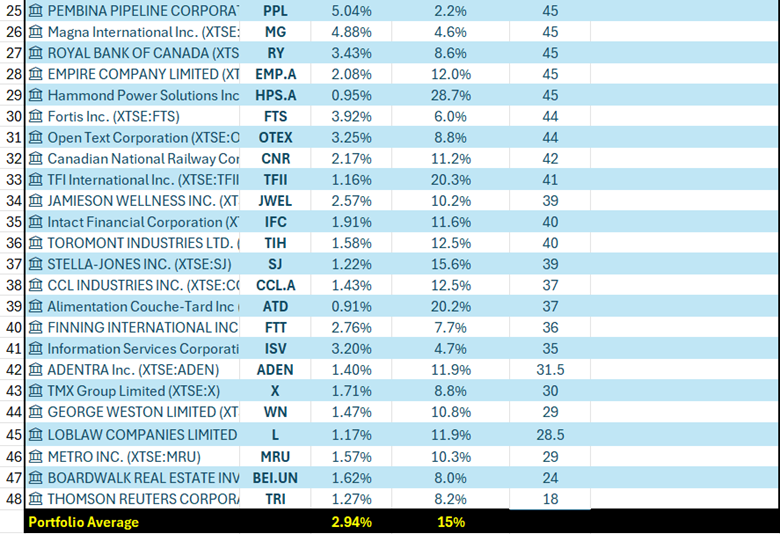

Here are the 48 that made the list:

Discussion:

What I like about this list is that its quantitative approach has put some names I would normally ignore onto my radar. Take Dynacor for example. It’s an ore processing service with a surprising history of strong returns and dividend growth. I would never have looked at it. Same goes for TWC Enterprises, which owns golf courses, Wajax Corp, an industrial supplier, and Jamieson Wellness, the vitamin company. Dividend growth stocks are a diverse and surprising group.

Plenty of inclusions are unsurprising of course. Take the prevalence of oil and gas companies near the top of the list for example, with Canadian Natural Resources, the highest-quality oil sands producer, taking the top spot. Canadian banks, grocers, rails, pipes, utilities, and insurers are all well-represented as well.

Eagle-eyed readers will have noticed some omissions, like Bell and Telus, Enbridge and TC Energy, and some banks. This is mostly because their payout ratios are too high right now. For Bell and Telus, there seem to be additional regulatory headwinds, and compared to National and Royal Bank, I don’t think the other banks currently compare. Feel free to disagree.

If I’d found a fair way to include special (irregular) dividends, companies like Algoma Central (a shipping company), Tourmaline (a natural gas company), and E-L Financial (an insurer/holdco) would probably rank much higher than they already do. Readers can incorporate that into their interpretation of the data as they wish.

Notably, this list features a lot of long-term compounders. TFI International (trucking), Equitable Bank, Element Fleet Management (logistics), MTY Food Group (quick service restaurants), and others, have all not just grown their dividends strongly but seen impressive share price appreciation as well. Dividends don’t have to be a trade-off.

If an investor were to put $10,000 into these stocks in equal amounts, their starting yield would be ~3%, or around $300 per year. That dividend could grow around 15% annually, if past is any pretense.

Here’s how the numbers would shake out:

Investors would, ten years from now, be receiving triple their original dividend payment at ~$1,200 for a yield on their original purchase of ~12% instead of the 3% in the first year. Here’s how that looks visually:

This, I contend, is pretty good, especially if you’re a retiree or near-retiree whose alternatives include bonds and GICs that will consistently reset near the prevailing interest rate. Is this a realistic outcome though? I’m not sure, but it’s certainly something to contemplate.

Conclusion

Dividend growth stocks are attractive investments. However, as a young person trying to accumulate for the future, who doesn’t need additional income or much psychological support to avoid bad financial decisions, I think the opportunity cost of buying dividend stocks exclusively is too high. Being willing to miss the next Constellation Software because it doesn’t grow its dividend is a trade-off I am unwilling to make.

In the future, when/if I have “enough,” would like more income, and can afford the opportunity cost, I think dividend growth stocks are a wonderful idea because their payouts grow over time while fixed income doesn’t, rarely would selling the dip be required, and they get great tax treatment (for now). I’m not at that point but will contemplate it when/if I get there.

The only situation that would cause me to consider dividend growth stocks exclusively at this point is if I were to borrow money to invest in equities. As discussed earlier, leveraged Canadian income investors get a tax refund, which, combined with their dividend payments, can cover the interest on the loan while they benefit from the compounding effect, in much the same way as folks who have investment properties have tenants paying the mortgage.

Is it as simple as that? It can’t be, right? It might be. I’ll discuss it in the next post on leverage and dividend growers: “Is Leverage Actually Bad?”

Great article. This is such a polarizing topic. I think most spend time trying to convince others (and themselves) that there is a mathematically optimal way of doing things and ignoring the psychology behind it. Leaning into the psychology of not having to sell is very on point. Good stuff.

Nice article Stephen, very informative on the subject. What about the increase (hopefully) of the stock price itself during the years one builds-up his/her dividend growth portfolio? For instance Dynacor stock price more than doubled during the past decade, is this not an extra benefit to the income investor who selects quality dividend growth companies? I do not see this point mentioned in similar articles or by dividend investors. Am I missing something?