Thermal Energy Int'l - Multi-Bagger Potential Helping Industry Go Green Profitably - TMG.V

Thermal Energy Int'l - Multi-Bagger Potential Helping Industry Go Green Profitably - TMG.V

Fast growing, profitable, insider owned, secular tailwinds, reasonable valuation

TL;DR

Introduction

Thermal Energy International is a fast-growing and profitable microcap company providing end-to-end fuel efficiency solutions to large industrial clients like Kellog’s, Pepsi, and Goodyear. TMG has a market cap of $46M CAD and trades on the Toronto Venture Exchange for ~$0.27/share at time of writing.

The Opportunity

When people think of green technology or carbon reduction we tend to think of solar panels, windmills, and electric vehicles. “Greening the Grid” or driving an EV is important for reducing greenhouse gas emissions; however, it has limited impact on industrial factories and plants.

This is because, according to TMG’s investor deck, 90% of energy used in industry is thermal (read burning fossil fuels), while only 10% is from electricity. Moreover, of this energy created thermally, 50% is lost as unused heat.

To put this in perspective, industry constitutes 25% of greenhouse gas emissions globally. A full quarter of the global economy goes unaddressed by focusing on decarbonising electricity.

With fuel prices becoming increasingly volatile (remember 2020-2021?), fuel supply getting less reliable (eg Russia supplying Europe with most of its natural gas), carbon emissions becoming a real government-regulated cost (especially in Europe), and many companies having made promises to stakeholders to meet certain carbon reduction targets, businesses no longer want to reduce emissions because it’s a good thing to do; corporations want to reduce emissions because there is a business case to do so.

Thermal Energy International has positioned itself to meet these the industrial carbon reduction needs (not wants) of large corporations.

The Case for Thermal Energy International

Put very simply, Thermal Energy International takes unused, excess heat and finds ways to make it useful.

Here’s a very simplistic and fictional example:

You’re Kellog’s and you’re making Rice Krispies in two vats. You burn natural gas to generate heat which you use to pop/toast the rice. 50% of that heat is dissipating - shoot. TMG’s sales guy has been pestering you for years and finally you decide to hire TMG to come in and figure out how to improve the efficiency of your vat situation.

TMG finds a way to capture the excess heat and redirect it from one vat to the other, so they sort of heat each other, reducing the overall energy required – they say efficiency will rise from 50% to around 90%. You agree on a fixed price that provides you a high ROI, then TMG does all the engineering, provides the products, orders what you need, and installs the whole thing. You just sign the cheque.

TMG leaves and your fuel bill arrives. It’s 20-30% less than it was before, meaning in 3-5 years you’ll have saved an entire year’s worth of fuel. Kellog’s is now more profitable, more green, more insulated from volatility in the price of natural gas and less exposed to the increasing price of carbon. You go to your investors/board/government and tell them just how great you are and graciously accept your well-deserved promotion.

There are probably far more realistic examples, but this is how I broadly understand what TMG does.

In list form, here is their value proposition to clients, most of which you probably inferred from the example above:

Custom Projects (“Bespoke”)

Each project starts from scratch with custom design for each site.

End-to-End Service (“Turn-Key”)

Meaning they do everything for the customer, from engineering, ordering, supplying products, and installing – ie they are convenient.

According to the CEO, no other company currently offers this level of service.

10 “Unique and Proprietary” Technologies

According to the CEO, other companies in the space offer a few technologies, but no one is close to 10.

Fixed Prices – High ROIs

TMG works with the customers to find a price, based on the customer’s own estimates of fuel prices, that will provide a short payback and high enough ROI to make the investment worth it.

Once agreed, they don’t change that price.

Can usually increase efficiency of operations from ~50% to ~90%

Leads to savings of 10-30% for customers.

Demonstrative of TMG’s expertise and experience – takes a lot of time to consistently get these results, especially when each project is custom.

Put simply, the value proposition boils down to TMG being competent, convenient, and cost-effective at putting unused heat to work.

The pitch to investors is that this nifty package is very difficult to duplicate and currently unique in the market. To their credit, from my own brief search for peers, I’ve found mostly companies do the engineering only, or products only, and none that looks like they do it all, as TMG seems to.

This is further reinforced by the fact that 80% of TMG’s business is derived from repeat customers. Why would you come back for more if you weren’t getting value? Additionally, if we go back to 2009-2010, when the current CEO took over, the company has grown sales at a 20-30% CAGR, suggesting high demand for their services. Looking forward, the company currently has a record order backlog and record Project Development Agreements underway, 150% more than before Covid.

Something is working, and that makes TMG very interesting.

Getting Critical

My immediate thought is that the business generates project-based revenue. Recurring revenue, like subscriptions or maintenance, is usually preferred as it is much more predictable and certain.

Allaying this concern is that while their revenue may not be recurring, their customers are. As mentioned earlier, 80% of their business is repeat customers, so theoretically if these customers have a lot more sites, TMG could have a lot more revenue to come.

This appears to be the case. According to TMG, their top 10 customers have 1,000 industrial sites worldwide and TMG have partially penetrated about 100 of them, completing around 5% of the potential work that could be done. With 95% of their largest customers’ work left, future revenues look predictable, even if they’re not technically recurring.

Significantly, the top 10 clients make up only 60% of orders, so there’s a whole other 40% of existing customers from which TMG could get more orders, in addition to the numerous other industrial companies that TMG does not currently work with. Quite simply, where there’s a factory or plant that produces heat, TMG has a potential customer – the addressable market is immense.

A second concern I have is around the necessity of their products and services. A factory doesn’t need to get greener/more efficient, even if there is a good business case to be made for it. If capital spending was just an ROI calculation, there may be higher priority plans for spending the money. Better energy efficiency might get passed on for robots or an expansion, hurting TMG.

The CEO mentioned in an interview that he thinks carbon reduction spending is becoming priority capex. It doesn’t surprise me he thinks this given his role and perspective, but he said that increasingly companies have separate carbon reduction capex budgets. Since budgets exist to be spent, TMG may be able to expect more consistent project funding with lower minimum ROIs required (hurdle rates) to approve projects. More money spent more liberally on carbon reduction projects would certainly benefit TMG.

He also said that it used to be the case that each site had its own capex budget it would choose how to spend. Whereas nowadays, orders tend to come from corporate headquarters, especially on carbon reduction spending. As a result, TMG has been able to get orders for multiple sites at one time by selling to corporate headquarters directly, which was not possible in the past. This again suggests favourable trends in TMG’s favour.

I didn’t want to take the CEO at his word as he may be trying to promote his company, but I think the chart below supports the CEO’s comments. It shows the number of companies with net zero commitments; we can see that it is increasing quite quickly

If this is indicative of corporate attitudes towards green spending, then the CEO’s comments are probably fairly accurate. All in all, I think we can reasonably infer that carbon reduction spending is becoming less optional and more streamlined.

I haven’t been completely placated by these answers to my more critical thoughts, but TMG’s weaknesses are certainly becoming less weak as long as their customers keep buying, green capex continues to become higher priority, and corporates continue to centralize their decision-making.

Building Trust in the Future and CEO

The CEO has suggested that order backlog (orders received that have not been turned into revenue yet) is a rough proxy for sales in 12 months. I decided to put this to the test by going back through MD&As to find out how much can we infer from backlog and how much we can we trust what the CEO says. What I found was assuring.

Backlog turns out to NOT a good proxy for sales 12 months later – because sales are usually MUCH HIGHER than the backlog (either at the end of the fiscal year [May 31] 12 months prior, or at the reporting date of that fiscal year).

On average, sales 12 months later were 66% more than the backlog at the end of the fiscal year, and 28% more than the backlog at the time of reporting.

This says to me that the CEO is being conservative with what he says and managing expectations. Personally, I love that he is not promoting and overestimating the future. He could pump the stock much more than he is but chooses not to. I like this.

The only instance I can find where he departed from his narrative was during an interview with Kyle Grieve on The Investor’s Podcast. It’s interesting because he had already addressed the order backlog data earlier but specifically circled back to it here:

“Just to help your listeners,” he says in an uncharacteristically, then says that in 2019 they had $22M of orders that resulted in $25M of revenues, while fiscal 2023 has had $27M in orders with $10M more at the time of their recording (Nov 2023). “So that gives you a little bit of an idea what the outlook looks like,” he finishes it off with, leaving us to read between the lines (We’re doing amazing). He seems to acknowledge, albeit briefly and reluctantly, that my little back test was right, and the future is a lot brighter than he’d prefer to say publicly.

Confirming my hunch is the record of insider purchases. As recently as February 1st, 2024, the CEO bought $100,000 of stock at ~$0.27/share in the open market for his RRSP. Considering he is paid $300,000 per year and owns shares worth ~$2M, this is a meaningful sum.

Whereas most CEOs are more talk and less walk, Bill Crossland seems to be more walk and less talk. I’ll be keeping an eye out, but he’s made a great first impression, to say the least. My confidence in the company has grown.

Valuation and Future Return Potential

Thermal Energy International has strong sales visibility, as it publishes the size of its order backlog and number of PDAs (project development agreements). Here’s how to estimate near term sales of TMG:

We know backlog is a conservative estimate of sales in the next year. In addition, ~75% of PDAs will become orders (according to known under-promiser Bill Crossland) and eventually revenue 24 months after they were initiated.

The average order is for around $2M, so we can estimate sales in the next 24 months by taking the number of PDAs, times 75%, times $2M, then add the current backlog. Here’s the calculation visually:

And thus investors can arrive at a conservative estimate of the near future. I used this method for the following valuation perspectives.

Firstly, here is TMG by ratios:

The result is that even if we use the most conservative method of estimating growth, the stock looks undervalued on a PEG basis; it is cheap relative to its growth, suggesting the CEO is right, and now is a favourable time to buy.

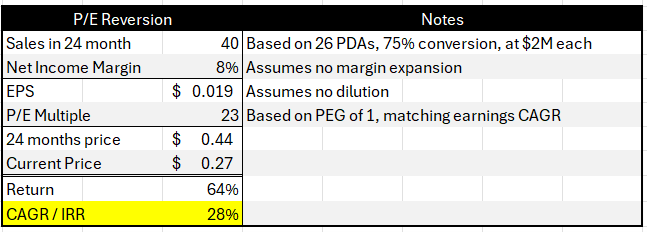

Here is a version where I just estimated earnings out a couple years and applied a multiple:

Even taking the same conservative sales growth, assuming no more margin expansion (even though it has been expanding), and a multiple like today’s, we still get a very attractive IRR for our money.

To judge upside and downside I did a “What if…” table to test what annual returns would be if we vary the profit margin and P/E multiple:

There are a lot more scenarios where we make more than 28% annually than there are less than that, and very few situations in which returns are negative. There appears to be a fair margin of safety built into the current price.

These are imperfect models though; they exist just to get an idea of possibilities and probabilities. Based on my best conservative guesses, the stock appears undervalued. The reality, however, could be drastically different.

Conclusion:

I think it’s time to zoom back out.

We’ve got a company that does really useful stuff, really well, has a lot more runway in which to grow, and record number of orders piling up. It benefits immensely from societal trends and the seemingly high integrity CEO is more bullish than he feels comfortable saying. Despite this, the stock seems undervalued even using assumptions of growth that are known to underestimate reality.

Overall, this stock looks like it’s going to reward shareholders with at least a double or two in the next five years, and maybe much more if this story continues.

I have it as a 1% position in my portfolio and will be looking to add when possible.