Pinetree Capital - A New Flavour of Constellation Software - PNP.TO

Software investing holdco with activist tendencies, Mark Leonard's children, and Constellation Software veterans.

Introduction:

Thanks to FinTwit, Pinetree Capital came across my radar. PNP is a ~$50M market cap investment holdco 33% owned by Constellation Software founder Mark Leonard’s kids, with one, Damien Leonard, running the show.

Joining in April 2021 is Shezad Ohkai, now 4% owner of PNP, a U of T comp-sci grad, former Bain Capital consultant/manager, and with 10 years experience at Volaris (an operating group of Constellation Software), which culminated in him as vice-president.

Constellation Software needs no introduction, but just in case, they are a serial acquirer of small, niche software companies (“Vertical Market Software” or VMS), and are really, really, good at it:

In total, Constellation has made over 1000 acquisitions and compounded at around 35% per year - a 210-bagger since 2006. Point is, Constellation knows how to invest in VMS businesses, so when the founder’s son and a former VP establish a new vehicle for doing just that, you get interested.

The Business

Here’s how PNP describes themselves, with the highlighted bits being what I think is important:

Here’s a summary of what Pinetree does:

To no one’s surprise, they are investing in software companies on a fundamental basis with an eye to intrinsic value (like Constellation).

They take minority stakes in 8-12 companies at a time (whereas Constellation buys businesses outright).

PNP eventually sells those stakes to realize gains (whereas Constellation never sells but collects and reinvests cash flows).

PNP is willing to be an activist investor, taking seats on the board of portfolio companies and providing advice where necessary (whereas Constellation has no need for activism because they own the business wholly).

I think of this company as a publicly traded activist hedge fund focusing on VMS businesses with the knowledge and experience of Constellation Software behind it. Overall, appealing at first glance.

Unlike hedge funds though, it doesn’t charge fees but does have expenses at the Holdco level, which look to be around 2% of book value annually.

Considering they only pay salaries to the CFO and CIO, Leonard takes no salary, directors get nominal fees (in the 4-figures), and the company’s registered address appears to be someone’s house, it seems safe to say they’re doing their best to keep that expense number down. Moreover, as book value increases, expenses as a percentage of book value will likely trend down. This might be the only hedge fund-type entity that tries to lower fees/expenses.

Another appealing aspect of PNP is that it has a sordid history as a money-burning mining speculator, before being repurposed by Damien Leonard. This is a good thing because it means PNP has $400M in deferred tax assets (DTAs). In other words, PNP is entitled to $400M in tax-free gains, while the current market cap is only ~$50M, meaning PNP can 8x before it must pay tax.

But does their strategy work? Buying stakes in discounted VMS businesses and sometimes helping them turn the ship around? Well they seem to be 1/1, if the current turnaround at portfolio company Bravura is anything to judge them by.

In the middle of 2023, Shezad Okhai accepted a temporary contract position (ending June 30th 2024) as “Chief Commercial Officer,” and Damien Leonard has taken a seat on the board. You can see that this coincides with the precise bottom in the stock. This suggests to me that Pinetree Capital’s activism can be material. Tristan from Hurdle Rate covers this well here.

Rather than create my own tracker of their portfolio, I borrowed this recent (March 1st, 2024) table of their holdings from Nicoper, who writes excellent articles for Seeking Alpha, especially on CSU, and whose twitter account you should definitely check out.

They have some high-quality businesses in there, like Signity, Topicus (both Constellation Software related), and SS&C. They also have some clear turnaround targets other than Bravura, like Quorum (QIS.V):

Which they seem to have begun to do something about:

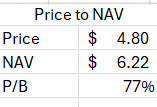

Another thing to consider, which some readers will have noticed, PNP.TO currently trades at ~$4.90, equivalent to the value of their portfolio in December 2023 (book value, BV). However, that value has increased substantially since then, to $6.22 per share, implying PNP.TO now trades at 0.77 Price to Book, a discount of 23%. Considering Constellation, Lumine, Topicus, and Sygnity are all trading extremely richly, PNP.TO at a 23% discount to book looks relatively inexpensive.

This basically sums up the bull thesis for this company. But there are counter arguments:

Firstly, is there any advantage to buying Pinetree over Constellation Software itself, or any of its publicly traded subsidiaries? In my opinion, I’m not seeing much of an advantage beyond the valuation. Why be an activist investor when you can just buy the whole thing? Then there’s no need for board seats and politics. Being an activist seems like simply a weaker form of ownership.

Additionally, having to realize gains (sell holdings) to raise capital for other opportunities seems potentially difficult to replicate consistently. If you invest in PNP, you’re really trusting Damien and Shezad to be able to time their sells, a notoriously difficult skill on which an investor in Constellation Software or its subs doesn’t have to rely.

For example, in 2023 they sold some Sygnity because of valuation concerns and position sizing:

Admittedly, the tax implications of selling are negated because of the deferred tax assets, but to me, Sygnity, being the smallest of all Constellation entities, is potentially the most attractive so I don’t love that they sold some, even though it was just a trim.

Rule #1 of investing in Constellation Software is never sell. Even if this sell call by PNP turns out to be the right decision in this case, how much can we rely on that success to be replicated? I don’t know.

We also don’t know much about Damien Leonard. I found a press release saying he has 15 years experience investing in VMS and can presumably just ask his Dad for advice when needed, but it’s still a question mark.

To Summarize:

I like:

Insider Owned – 33% owned by Leonard Family, 4% by CIO.

The people and their skills – Constellation Software playbook and veterans.

The structure – low fee specialized activist “hedge fund.”

The DTAs – they can 8x without paying tax.

Focus on keeping expenses low.

23% discount of book value.

I don’t like:

That other Constellation entities are probably better vehicles for compounding.

Activism is probably inferior to just buying a business outright.

They must opportunistically sell holdings to raise capital to reinvest rather than just collect cash flows.

Adds another step that is potentially difficult to replicate successfully.

Not really knowing much about Damien Leonard.

Conclusion:

There is a new way in town to gain from Constellation Software’s skill set and playbook. Is it better than the existing ways, namely TOI.V, LMN.V, CSU.TO or SGN.WA? Unless you emphasize valuation, I don’t think so.

That said, I would wager PNP beats the market and if Leonard’s and Ohkai’s portfolio management is up to snuff, they probably outperform their holdings as well.

I’m already very overweight Constellation Software entities so if I wanted more exposure and the entities I hold get to real nosebleed valuations, I might consider adding PNP.

Currently have no position.

Thank you for this story. Some follow up questions.

What is the most current NAV only related to Public companies ignoring illiquid private positions?

How did Management increase NAV since taking over this vehicle?

What are unique characteristics of some of the larger portfolio positions?

My big concerns are suboptimal AUM and ability of management to compound capital and to a lesser extent risk of management self dealing.