NTG Clarity – High Risk Nanocap with PEG of 0.03 - $NCI.V

Growing 100% profitably at P/E of 3, but with a lot of "buts"

TL;DR

There is also a bullet-point summary of the research if you scroll down a bit (has a heading).

Introduction:

Headquartered in Toronto, NTG Clarity Networks is a ~$15M market cap IT services provider to a variety of industries and primarily to companies operating in the Middle East, Saudi Arabia in particular. It’s 45% owned by insiders and showing signs of life 25 years after the dot com bust.

The stock rapidly doubled off lows recently:

Why Now?

NCI.V crossed my radar recently because of a Wolf of Oakville Fins Review that seemed simultaneously too good and too bad to believe.

The company, in a news release, suggested they were on track to double sales (from ~$25M in 2023 to ~$50M in 2024) at a 10% profit margin. This implies $5M of net earnings, for a 2024 estimated P/E of 3… while growing at 100%. I’d never seen a PEG of 0.03, but now I have.

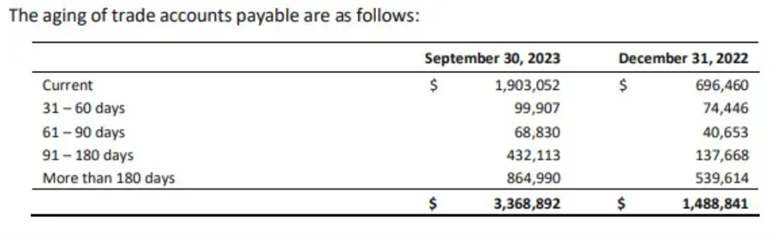

At the same time, the balance sheet looked as bad as the growth looked good. Current liabilities are greater than current assets (meaning they’ll have to borrow in the short term to meet commitments). Moreover, they seem to have great difficulty paying people on time, with significant accounts payable over 180 days:

Furthermore, debt is sizable at around $6.5M but that’s not supposed to be too concerning because it’s owed to the CEO himself, who has not imposed repayment terms and is charging minimal interest. The CEO also hasn’t taken a salary for years. That’s great, but I expect eventually the CEO will need to be paid back, however.

Overall, this is a tale of two financial statements: an Olympic-calibre income statement, and a beer-league balance sheet.

I decided I needed more info as to how this could be, so I did a couple days of learning and thinking about it, and had a discussion with Adam Zaghloul from NTG Clarity. The details I found are, like the financial statements, a mixed bag. I had a hard time sorting it all in a way that made sense, so I just did a brain dump:

Brain Dump

The first thing to note is that the company has a twenty-year history of hamster-wheeling from growth and profitability to shrinkage and losing money. But recent history (the last 10 quarters or so) has been consistently profitable and growing. Investors must figure out if this recent trend is sustainable, or if this is NTG Clarity doing what it’s always done.

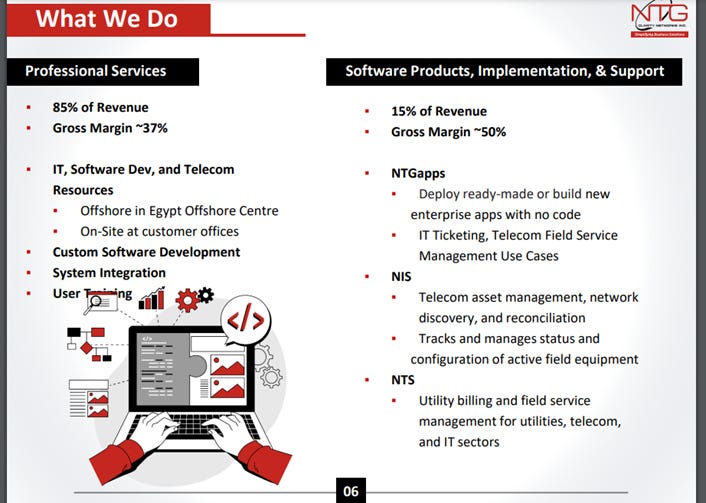

The company would argue no, of course; recent performance is fundamentally different from the past. This slide tells us why they think that:

First thing to note, is that the claim of “Never-Before-Seen Growth” is true. The company has never had more than $15M or so in sales, but they will be breaking through that barrier with around $25M in sales in 2023, with a backlog (unbilled projects and orders) now over $40M, as of March 27th 2024. Management’s 2024 estimate of $50M in sales is credible. Overall, something does seem to have changed at NTG Clarity.

The first bullet on slide from the investor presentation mentions expanding IT services to the financial sector, and notes that the Kingdom of Saudi Arabia (KSA) is eating this up. Rooting through MD&As, I found that the Saudi’s expanding interest in NTG’s services is showing up in the numbers, with sales up 150% year over year:

In addition to the impressive growth, they appear to be getting significant repeat business, along with new customers. Saudi seems to love NTG Clarity.

The second bullet mentions the introduction of an Egypt Offshore Centre. This video was helpful in understanding what that means:

It sounds like the inverse of on-site services. NTG has a bunch of Egyptian IT/software people doing projects from a hub, rather than flying in and staying at the destination. This saves customers and the company money. That, at least, is my understanding.

The Offshore Centre model is working well, as we can see from the financials and the fact NTG is opening another one in Cairo as we speak. I wondered, however, to what extent this business relies on the Egyptian currency being weak. Are the Offshore Centres economical because NTG can get paid in a strong currency and pay employees and other expenses in a hugely devalued currency?

Adam Zaghloul from NTG Clarity said this is not the case; the business model can stand on its own. The main difference of the currency situation, in his opinion, was that they are slowing down efforts to make more Egyptian sales because the currency is in freefall. I also asked Adam about the scalability of the model, and he said that even with all the new contracts announced they haven’t filled the new office, so there is capacity to spare.

To get a sense for the currency devaluation context in Egypt, the revenues NTG attributes to Egypt grew on an FX-neutral basis by 36% year over year, but when converted in Canadian dollars, sales shrunk.

For a company to grow that much and still “shrink” after currency conversion shows just how much the Egyptian pound has fallen.

Investors could look at this as positive, that adjusted for FX, the business is growing faster than it looks on paper and can take advantage of relatively cheaper labour and expenses. On the other hand, this could easily be viewed as evidence of instability in the business because of the country in which it’s operating. Much like their financials, these details are a mixed bag.

A similarly double-edged story is told in the revenue mix. I only have the numbers for 2022 since 2023’s year-end MD&A isn’t out yet, but here’s how it looked then:

Saudi counted for 60% of sales in 2022 and has probably increased as a percentage given the 150% growth year over year mentioned earlier. Again, we have a double-edged sword where on the one hand it could be seen as positive to have high exposure to a country digitizing and diversifying so rapidly, but on the other hand to be so concentrated in a country whose economy is still dependent on the price of oil and has autocratic leaders is clearly a risk.

A recent expansion into Iraq could be viewed by investors as an example of what I think may be a niche for NTG Clarity. The Egyptian Offshore Centres are filled with trained IT/software professionals who are native Arabic speakers and can likely relate easily to their middle eastern customers (Egyptian Arabic is a good one too because it is intelligible across dialects as it is central, and Egypt is known for its widely viewed media like music, movies, and TV). In my experience, being able to relate culturally and linguistically to people is a lot more solid of a barrier to entry than it appears.

In short, not a lot of companies could do business in Iraq, but then again, maybe not a lot want to. It may sound naïve, but NTG Clarity’s familiarity with the culture, people, and language of the middle east is likely a competitive advantage, but not without risk.

Eagle-eyed investors will that there is a Canada segment however, and would be pleased to know that Canada segment has doubled year to date over the same period in the prior year:

Unfortunately for investors seeking less geographic/political risk, this does not mean NTG Clarity is doing much business in Canada. What it means is that the Canadian office is bringing in revenue, mostly from, you guessed it, Saudi Arabia. Though diversifying revenues streams is a priority, Saudi continues to be the main customer.

Additionally, there is a proprietary SaaS platform they’ve developed, “NTGapps.” It is trying to provide low-code software templates for enterprise solutions, like IT ticketing, asset management, billing, inventory tracking etc. I downloaded it, but it seems that the app available for consumer download is front-facing, and I couldn’t do much. It did have good reviews though. Regardless, NTGapps sounds to me a lot like Canva, but for business app development, I could easily be wrong though.

As of November 2023, NTGapps made up 15% of their revenue, and had high margins. Yes, just about every remotely technological company has a SaaS offering, so I take it with a grain of salt, but it’s not the main reason to invest in NCI, NTGapps is a free option, so I’d take it if it’s there.

Lastly, it’s a bit strange that the CEO owns shares and the debt; investors might wonder what type of incentives that creates. I wanted to highlight the “Wolf of Oakville’s” take on this, as I thought it was insightful. He said in the CEO.ca chat:

“I’m not saying the situation is ideal, far from it. That loan WAS with a bank (RBC if I recall) and [NTG] was in default, so the two leaders absorbed [the debt] to keep the company alive. Those same leaders haven’t been collecting a salary for quite a while it appears… There are a ton of leaders on the venture who would be handling this much differently to shareholders’ detriment. They could have settled that debt and restructure it at 12 points, which is more the norm in TSXV land – they didn’t. They also funded the entire PP, could have issued warrants with the raise – they didn’t. Could have tried to raise more with outside capital and paid themselves salaries – they didn’t.”

We end up back in double-edged sword land – management has displayed high integrity but the opportunity to demonstrate it was only brought about because the business was in default.

Additionally, they did a dilutive private placement this past December to shore up the balance sheet and invest in growth, but the stock was trading at lows and management thought the stock undervalued. This was a debatable decision that turned off some investors and was supported by others. I discussed this with Adam, and I suggest you do to if you have any questions (on anything). He is candid, open, and responsive, which is refreshing for investor relations.

My two cents, I don’t like giving banks special treatment and think that the stock of companies that treat all shareholders well do better over the long-term, as they attract a quality shareholder base who can hold through bumps in the road. Where there is low shareholder turnover and high management execution, there is multiple expansion.

Here’s a summary of the research:

NTG Clarity has a bad history but a great recent history.

The balance sheet is as bad as the growth is good.

The high debt-burden is owned by management, which is better than an outside creditor, but will have to be paid back eventually.

Growth and profitability have been unprecedented, but most of it is coming from Saudi Arabia and happening in Egypt, which comes with risks.

Offshore Centres in Egypt are driving a lot of the profitable growth, for which a weak local currency is a tailwind, but management suggests is not necessary to be successful.

Recent business in Iraq may be demonstrative of a competitive advantage stemming from cultural competency… and/or a high tolerance for risk by management.

60% of sales come from Saudi Arabia, and the 12% coming from Canada also came largely from Saudi Arabia.

Investors get a free option on a proprietary SaaS platform for low-code enterprise software development called, “NTGapps.”

Management has shown high integrity in the past, but only had the chance because they had defaulted on their debt.

Management raised dilutive capital in December to shore up the balance sheet and invest in growth – at lows and a big undervaluation.

Those are the facts, as I see them - there is risk here but also opporunity. With that established, let’s explore the reward side of the equation now to see if an investment in NCI.V is worth it.

Valuation and Return Estimator:

To buy a nanocap turnaround like this, I’m going to need the potential for a big reward. Firstly, here’s a reminder of the implied 2024 P/E and PEG assuming management’s 2024 guidance is not hopelessly optimistic:

This is a pretty absurd PEG and might be totally irrelevant (but might not…).

Secondly, I got an idea of potential return by estimating sales a couple years from now, applying a profit margin, dividing the resulting profit by shares outstanding to get Earnings Per Share (EPS), and applying a variety of possible P/E multiples to that EPS:

Personally, I look at the potential CAGRs and think the risk is probably proportional to the reward, numbers-wise. If this company reverts to low growth and no profit, investors could lose, but I think that is less likely than in the past, based on my analysis in the previous section, particularly because of the changing business model and growing backlog.

I’ll let investors substitute their own assumptions, but valuation exercises like these are always at best a sketch, more to get a sense of the probabilities and possibilities, than to make or break a decision. My final decision will always be based on an analysis of the all the facts, not just an attractive-looking spreadsheet.

Conclusion:

I’ve never been more conflicted because NTG Clarity Networks is simultaneously one of the worst and best businesses I’ve looked at. In what world does a company profitably growing at ~100% trade at a P/E of 3? Are the “buts” so large that this valuation is deserved? I’ll leave that up to investors to decide.

I love the income statement, dislike the balance sheet but believe it will improve, and consider the business on the risky side but well-positioned and overall, still don’t really know what to think.

I bought an absolutely miniscule position just to see what it’s like to own (I find that helps with decisions). I may or may not add, but it will never be a large position. If it works and I’m not a big part of it I won’t mind as it feels very close to going in the too hard pile.

I won’t stop checking it though, and will probably follow up with Adam later. My curiosity is certainly piqued.

Got a little lucky for it too happen and so soon! Thanks for reading

5 months later the stock has risen to 1,60. Absolutely mindblowing, it's a shame I read this article in August and not in March :'(

Amazing work. Thank you for all your content <3.