Mattr Corporation – Emerging Compounder at a Low Multiple?

Another industrial acquirer enters the arena

TL;DR

MATR wants to buy industrial businesses cheap, grow them at above market levels, generate a bunch of cash and reinvest it at high rates of return. They have an experienced CEO executing a practiced and proven playbook leading them, but a short track record, noisy financials, economic headwinds and a market that doesn’t know what to think about the company. Continuing to execute will draw in new money and increase certainty around management’s capital allocation skills, but it’s early days for MATR and their investors.

Introduction

Sometimes I make pizza dough from scratch. I follow the recipe precisely and when the dough is mixed and set down to rise, even though I know I everything is just right, until I can physically see the dough start rising, I’m never sure it will work.

That is how I feel about Mattr Corporation. It has all the right ingredients in the right proportions prepared the right way, but the proof that this will result in success has not yet arrived.

The plan in this article is to go over why this stock should work, and how to tell when it does or doesn’t.

Brain Dump

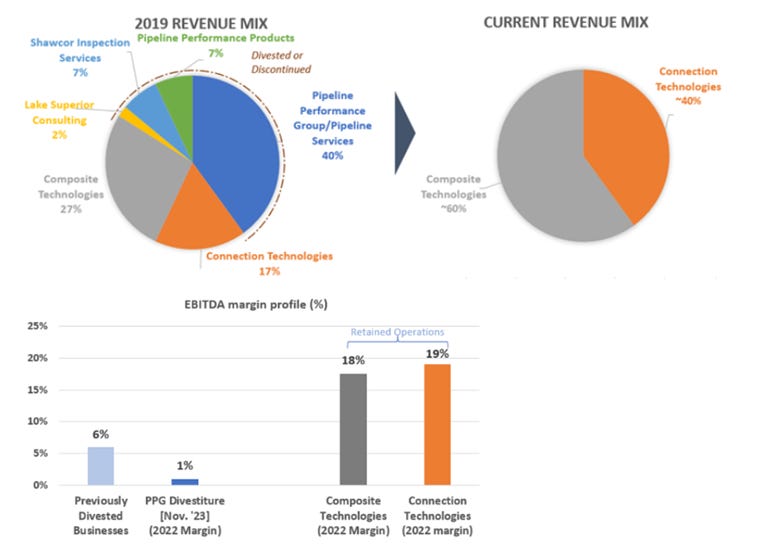

Mattr Corp used to be Shawcor, a company heavily exposed to the oil and gas cycle. New management was hired in 2021, who sold off most of the very cyclical businesses and added some smaller businesses to become more of an industrial materials supplier. The final piece of the transition is almost complete, with the recent announcement of the large acquisition of Amercable, a well-run wire and cable manufacturer whose customers are mostly blue-chip miners, for 5x EBITDA and is immediately 40% accretive to EPS. Something has definitely changed.

These are the company’s businesses post-divestments and acquisitions (borrowed from an excellent VIC write-up which I’ve updated):

To get a sense of the transformation that has occurred, here is how the revenue split has changed over time (again from the VIC write-up). This is pre-Amercable Acquisition, so the “Connection Technologies” segment is over 50% now. Notice how the retained businesses have much higher margins than those divested.

Management has also been investing in organic growth, spending a significant amount of capital on improvements in manufacturing, with the goal of growing organically at 10% annually into 2030. With most of this capex is behind them, investors are hoping to see operating leverage kick-in, free cash flow surge, and the stock get some love.

A significant piece of the capital allocation puzzle are share buybacks. The company has aggressively bought back shares in the past, reducing the share count from ~70.5m in 2021 to around 65m today. They have an open NCIB for 10% of their shares now, which a look into their filings reveals they’ve been using. Additionally, insiders (including the CEO) have been buying alongside the company.

Lastly, if this story is reminding you of every private equity turnaround you’ve ever heard of, management’s leverage goals will dispel this feeling. The company plans to keep debt at moderate levels, not going above 2x EBITDA for long. They describe the capital allocation framework I just highlighted as an “all of the above” strategy. It’s laid out cleanly here.

You can see why I like what’s cooking at Mattr. Aggressive buybacks, low leverage goals, capex winding down, double digit organic growth in the forecast, acquiring high margin businesses at low multiples with a 20% after tax hurdle rate, and insider buying – all green flags.

To use another tired cliché, this promising activity has yet to bear fruit, however. Margins have compressed below their long-term goal of 20%, FCF is almost negligible despite having 70% conversion targets, and revenue growth will be nearly flat year over year while management discusses 10% organic growth into the future. More on that later.

In the absence of hard evidence of success in the financials, investors can either wait and see (as many seem to be judging by the valuation) or do their own due diligence on the end markets for Mattr’s products and its management.

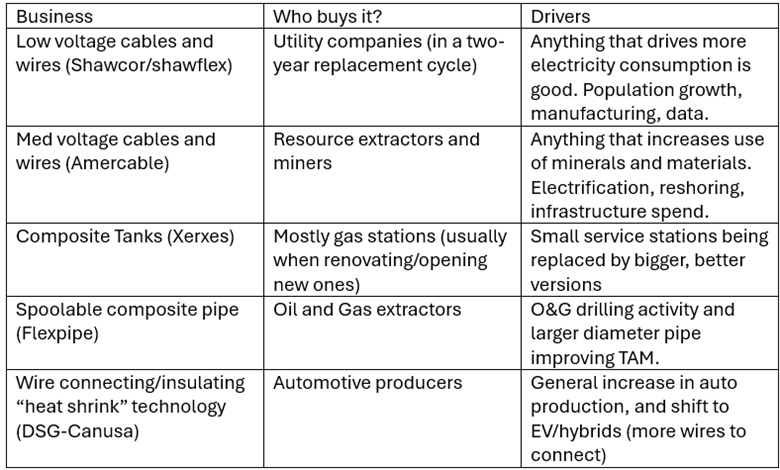

Mattr’s Products

As it this is a conglomerate with several products serving a number of industries, in relatively niche markets, it takes time and resources to do due diligence on this company. I don’t have that, but this is the framework I’m using:

The company claims many of its products are “highly engineered,” suggesting that this provides defense from certain competition. I think that’s probably true to an extent, EBITDA margins are fairly high (up to 20%) implying some pricing power, but I’m sure making something like a composite tank is not rocket science, and they do have competitors. I haven’t done enough work to have a strong opinion on any of these businesses individually, but these guys in this interview have:

I wouldn’t underestimate the businesses though, despite them sounding quite boring and mediocre. Interested readers should check out Amphenol (APH), an acquisitive company also in the wire and cable business that is a top-tier compounder. Check out its chart:

For Mattr specifically though, I generally think manufacturing is set for a recovery, and electrification and infrastructure spend is on the rise. This should help the industries Mattr supplies, at the very least.

Assuming lack of expertise on the individual companies within Mattr, to own the stock prior to proof of concept showing up in the financials, investors must have significant trust in management.

Management/CEO

Trusting management is a big part of the thesis at this point, and they look promising. CEO Mike Reeves has about as gilded a resume as investors could wish for; I honestly am not sure how tiny, old, Canadian Shawcor convinced him to join them. He has an engineering degree from the prestigious Imperial College of London (refreshingly not an MBA), honed his skills at blue-chip industrials Schlumberger and NOV, then led some private equity-backed businesses, the most recent of which he founded, “Rubicon Oilfield International.”

From 2015 until it was sold in 2021, Rubicon grew organically and by acquisition - a very familiar playbook to anyone who’s gone through Mattr’s investor deck. Significantly, Rubicon was backed by private equity giant Warburg Pincus, who made their reputation investing in industrial businesses, focusing on, you guessed it, organic growth and accretive acquisitions. It seems like Reeves may have picked up a few things and/or already been adept at them.

I didn’t know much about Warburg, but I’d certainly heard of their most well-known success story, the IPO of Transdigm. TDG has become an epic compounder in the industrial/aerospace business by way of above-average organic growth and accretive acquisitions (now a familiar playbook).

Another detail, the guy at Warburg who oversaw the investment in Reeve’s Rubicon Oilfield International lists it as one of his “investment highlights” in bios for some of his retirement projects, suggesting Reeves made him and his investors money.

Additionally, Turtle Creek Asset Management, a firm run by former private equity managers who have most of their own net worth in their own funds and focus primarily on quality midcap stocks with strong management, holds a significant position in Mattr Corp and have been adding. Turtle Creek owns over 15% of MATR’s outstanding shares, up from 12.7% a month ago (Sept 2024). In short, Turtle Creek’s experienced partners have their own money and that of their clients invested in MATR in a big way.

Management themselves don’t own a ton of the company, and the CEO owns less than four times his annual salary in stock. Not bad, but not “founder” level.

As a result, I looked closely at compensation to see if he would be more closely aligned with shareholders that way. Him and the whole management team have a big portion of their compensation related to EBITDA and free cash flow performance. Compensation related to fundamental improvement instead of stock price movement is welcome.

Additionally, in the YouTube interview with Clayton Partners from above, the managers on the call said that management have not been “net exercising” their stock options, meaning that they’ve been using their own cash to exercise options. Normally, management teams will sell some options back to the company to pay for the options (“net exercising”) but not so here; management apparently wants all they cheap stock they can get.

To me, it sounds like CEO Mike Reeves is the real deal, following a practiced and proven investment playbook, and there are others more qualified and experienced than myself who agree. He doesn’t have his whole net worth dependent on Mattr’s performance, but his incentives are aligned with shareholders, buys back shares, and has delivered value to investors in past endeavours.

Current Performance and Outlook

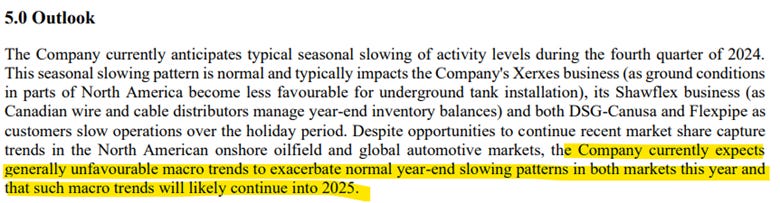

As I’ve alluded to throughout, the most recent quarter’s numbers were not exciting: flat-ish sales with lower profit margins.

There was a lot of noise involved as businesses are being divested and invested in all while the economy does its thing, so it can be hard to separate out reasons for disappointing numbers. Management says there are several one-time expenses related to the turnaround, lower utilization rates of the facilities (fixed costs are fixed unfortunately) and that the macro environment is quite unfavourable:

I’ll let readers go through the earnings calls on their own, but the important part is that most of the turnaround will be complete by mid-2025 (so 2026’s financials will be a lot cleaner), the businesses are performing as management would like (read the whole passage above to learn they are taking market share in fact), and that if the macro were to improve, the company is ready to capitalize. It’s up to investors to make a judgment on whether to believe them.

One thing I didn’t love is that management announced a big contract for Flexpipe due in 2024, but later had it cancelled, revealing they had never actually received the purchase order. I thought that was a little amateur, maybe it’s common in private equity to inform investors of likely but not certain developments, I don’t know, but the stock has been sliding ever since. Public markets hate missed expectations.

This price slide, especially in the context of a large, new, and good-looking acquisition, brings us to…

Valuation

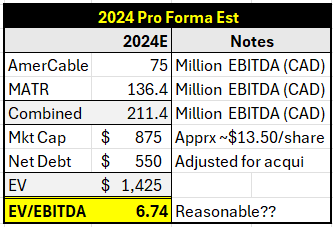

All figures are in CANADIAN DOLLARS.

To get accurate numbers we can’t look at reported numbers because they don’t include the recent acquisition. According to management, AmerCable did $75M (CAD) in EBITDA in the last 12 months:

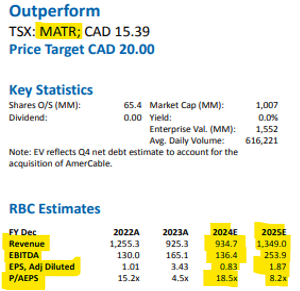

Analyst estimates for the full year of 2024 are for the existing company to do $136M in EBITDA:

This results in ~$210M in EBITDA if the companies had been one at the start of the year:

The multiple being paid for MATR right now looks very reasonable. Going forward, depending on how well investors think they’ll do next year, the stock looks even cheaper. It seems that they are not getting much credit for the acquisition or the turnaround.

Here’s how it looks through a FCF lens:

Again, it seems like the company is not getting a lot of credit. If this were a private company we’d be getting paid back in six years at the current price and targeted levels of free cash flow generation.

I also ran a simple DCF based on management’s guidance. It’s no wonder they are looking to buy back shares:

Note that this model excludes multiple expansion and future M&A. With multiple expansion (probably a product of execution) and any future M&A, the current price is history.

As much fun as it is believing management and putting assumptions into a DCF until you get a multibagger, the real value of DCF modelling for me is finding out what is priced in. In the following, I adjusted assumptions until I got a fair value estimate that was roughly similar to the current price:

It appears that the market is pricing in essentially no growth in sales or margins and higher than expected capex. Investors will have to decide what reasonable expectations are for the company, but now we know for sure the market has low expectations.

None of it matters unless the company executes, but there is certainly a margin for error and substantial upside if Reeves is as good as his resume.

Conclusion

Mattr rhymes very hard with TerraVest in 2014. That’s the year TVK finished the restructuring and did its first acquisition (at a very reasonably multiple and high ROIC, like AmerCable). Like TerraVest until recently, MATR trades at single digit multiples.

The biggest difference between the two is track record. In 2014 there was no way to know TerraVest was exceptional because they had not proven they could get good deals repeatedly and operate a business expertly. It took them ten years of proving it until the market really caught on.

Mattr still needs to prove themselves. With headwinds to their businesses, noisy financials, and a short resume thus far (Mike Reeve’s prior experience notwithstanding), it’s simply tough to know what the future holds.

That said, I like sidecar investing, ie finding companies led by great capital allocators and letting them do the hard work for me while I parent my kids, go to work, and play in my golf simulator with friends.

In sum, if Mike Reeves shows he’s got what it takes, I would love to hop in the sidecar of his motorcycle, especially at current multiples.

I own a starter position and will add aggressively if given a good reason.

Great write-up!

Great write-up.

I really like MATR at the current valuation.

I like how clear the plan is for management when you hear them talk about it. Disinvesting is done. Large production capex is done with expanding capacity. All of this while maintaining more cash then debt.

They’ve been wanting a US cable company that is buy-American compliant; now that’s done too. And at very attractive multiples.

Quarterly results and short-term guidance killed the Amercable momentum, but, as you mentioned, management could be way off their published 2025-2030 plan and investors would still earn decent return.

It’s an opinion, but think their is a very interesting upside with limited downside risk at this point.

To quote Howard Marks: « Price Matters More Than Quality. The key is the price you pay. You can buy the best company in the world, but if you overpay, it's still a risky investment. On the other hand, a lower-quality asset can be a great investment if you get it at the right price »