Hammond Manufacturing - Mediocre Business at a Great Price Relative to Comps - $HMM.A

But does smallcap value work?

TL;DR

Introduction

Hammond Manufacturing is a family business that’s been around for 100 years. In 2001, they spun-out Hammond Power Solutions, which led to my first question, “what’s the difference?” The best explanation I’ve found is from Hammond Manufacturing’s website:

In short, Hammond Power Solutions (HPS) makes fancy transformers, and Hammond Manufacturing (HMM) makes more typical (commoditized…?) electrical components. This may be our first hint as to why HPS has outperformed HMM:

Not that 450% is going to upset anyone though! Is there more in the tank?

Bird’s-Eye View:

Electrification, digitization, and aging power infrastructure have caused considerable demand for electrical components. Most recently, Covid, the power demands of AI, and the increasing threat of climate change have likely accelerated these existing trends. From a societal point of view, Hammond has the wind at its back.

Worm’s-Eye View:

From the bottom up, however, Hammond Manufacturing had an incredible 2021-2022, but 2023 was lackluster, and 2024 looks to be similar. From their 2023 annual report, here are their quarterly numbers:

As you can see, sales have dropped sequentially in recent quarters, hardly growing year over year. Operating income and EPS improved quite dramatically however with margin expansion.

To address why this was the case, here is HMM’s beautifully brief and highly candid letter to shareholders

On the negative side, half of the 5.5% sales growth was due to positive currency fluctuations, which could easily go against them this year, leading to disappointing numbers. They also acknowledge 2021 and 2022 likely saw a lot of demand pulled forward so a year or two like this could be expected.

On the other hand, I like that they suggest there was some operating leverage (getting more output from the same fixed infrastructure), that they raised prices in 2022 and found their customers willing to pay it (suggesting some pricing power), and that they are positive enough about the long-term to build another facility.

Management’s near-term view is not great however:

They see 2-4% growth this year, which could be made worse if the US dollar deteriorates in value (as they expect). Forebodingly, they say they are pricing their products competitively to stimulate market share growth. To me, this sounds like they might be accepting some lower margins in certain products for long-term gain.

For what it’s worth, nVent Electric (NVT), the market leader in products like HMM’s, does not have a grand view of the near-term either:

Like HMM, they see low single digit organic growth, with some pricing and productivity gains to try to maintain or expand margins.

Overall, because the near-term growth picture is not titillating, I don’t think investors have to rush to own this stock.

The Mountain-top view:

The best lens from which to view this stock, to me, is from between the bird and the worm, from the mountain top. Historically, HMM has grown sales at 10%, and margins have been improving so EPS has grown faster (20% 10-year CAGR). The business is slowly improving itself.

In addition, the secular tailwinds are accelerating. One needs only look at Nvidia’s earnings to see that data centers are growing like weeds. Looking out 5-10 years, I think you could expect HMM to grow sales faster than it has historically. If you add to that improved and/or growing margins this appears to be an attractive business to own, regardless of what’s happening next year.

To buy HMM today, I think you’re planning on owning it long-term, and not expecting anything dramatic to happen in the next couple years.

The Bull Thesis:

The bull thesis is best laid out by Smoak Capital here. To me is sounds like the pitch is “Medium-quality business at a cheap price based on comps.” Here’s a snippet:

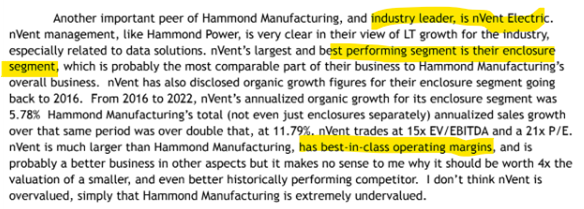

Essentially, Smoak Capital (who we should listen to because his returns have been excellent), is saying HMM is undervalued based on similar companies. In this snippet, he compares nVent Electric to HMM, noting that while it may be a higher quality business, it trades at a much higher multiple. Earlier in the pitch, he makes a similar comment when comparing Hammond Power Solutions (HPS) to HMM

Here is a summary using extremely rough numbers to get the point:

As we can see, HMM is valued substantially less than what appear to be reasonably fair comparisons. The main differences are that HPS is growing much faster and has more differentiated products, while nVent has much better margins. As a result, I don’t think anyone is arguing HMM deserves a 20x multiple or that HPS and NVT don’t deserve those multiples, just that 6.5x for HMM seems rather low. According to the bull thesis, HMM will re-rate, netting investors a return fueled by EPS growth and multiple expansion.

Bear Case:

Personally, I am not sold on the bull thesis for a few reasons.

The first is that relative to the best comparison, itself, HMM is trading in its normal range:

The valuation appears low for a reasonable quality business, but relative to the company’s own history, this is completely average.

A second reason I’m not a buyer at current prices (~$10.50/share), is because to get a worthwhile return (15-20% CAGR), the stock requires a re-rating and/or, improved sales growth and/or an improved margin profile. Here’s a basic return estimator demonstrating this:

As we can see, if the company continues like it has, investors won’t be getting anything special. Investors at current prices are betting some or all of these variables change going forward.

Below is a sensitivity analysis solving for the IRR, and varying net margin on the x-axis and the P/E multiple on the y-axis, so investors can look and see what type of annual returns they can expect based on what assumptions they have about the business:

Bottom line, to get an out-sized return at current prices, something would have to change positively, and it doesn’t look like that catalyst is going to be provided by the business itself. Investors at current prices must be expecting other investors to notice the discount to comparable companies, or demand for electrical components to increase more than expected, neither of which assumptions I’m fully prepared to invest in.

Conclusion:

Despite a big run-up, reasonable numbers, a solid-looking family-run business with secular tailwinds, and even a very successful sister company, HMM hasn’t managed to garner enough attention to re-rate. I don’t know why it would now.

It needs higher growth, or in the absence of that, an upgrade of its investor materials. If they trumpeted all the tailwinds that benefit its business, make a nice presentation, and start doing interviews (as HPS and NVT do), I think they’d have a better chance of re-rating.

I certainly understand those saying, “but the underfollowed are where the opportunity is!” and I agree generally, but in microcap I’m learning that attention matters. Microcap stocks can languish for years and years in the absence of substantial growth or a compelling story being told. I don’t think HMM has either.

Others do, like Thermal Energy International (TMG.V), Atlas Engineered Products (AEP.V), and even the 10-person operation at Fab-Form Industries (FBF.V), all of which are industrial microcaps that I’d buy over Hammond Manufacturing (HMM.A).

In the absence of better opportunities I might consider HMM, as there is nothing wrong with it, but for now I have no position, and am not planning to open one.