Cooper-Standard – Business Improves, Macro Doesn’t – Earnings Update $CPS

The multibagger potential remains, just slower than planned.

Introduction:

I borrowed this idea from Tom Hayes at Hedgefundtips.com, who in turn modeled the idea off Charlie Munger’s Tenneco trade. Peter Lynch did something similar with Chrysler. I wrote it up myself here.

Cooper-Standard is an automotive component supplier to most OEMs, especially GM, Ford, and Stellantis. The main idea of the investment is that there is pent-up demand for vehicles and Cooper-Standard’s impressive operating leverage and depressed stock price provide an opportunity to capitalize, as long as the company doesn’t go out of business in the meantime.

Since I wrote my first piece we’ve had some developments, so I thought it would be time for an update.

Credit Upgrade

By way of Tom Hayes, I learned that Moody’s upgraded Cooper-Standard’s debt rating:

Moody’s no longer thinks Cooper-Standard is at risk of imminent default. This is good news! The reasoning is more important, however. An entity that isn’t an investor in the company or the company itself is corroborating a lot of the positive developments we’re seeing. You can read the rest of the report here.

To sum it up, Moody’s says:

Earnings are improving

CPS is getting better prices from suppliers and customers

Costs are coming out

Leverage is still high

CPS make competitive products

CPS supplies mostly popular vehicles (so are more stable)

Newer businesses/product platforms are higher margin

Expect margin expansion despite lower production volumes

Liquidity, between cash and credit facilities, is sufficient.

Looking good to be free cash flow positive in 2025

There are some negative points, like auto production volume likely to soften and leverage still being high, but by and large, Moody’s thinks things the turnaround is underway at Cooper-Standard.

Q2 Earnings

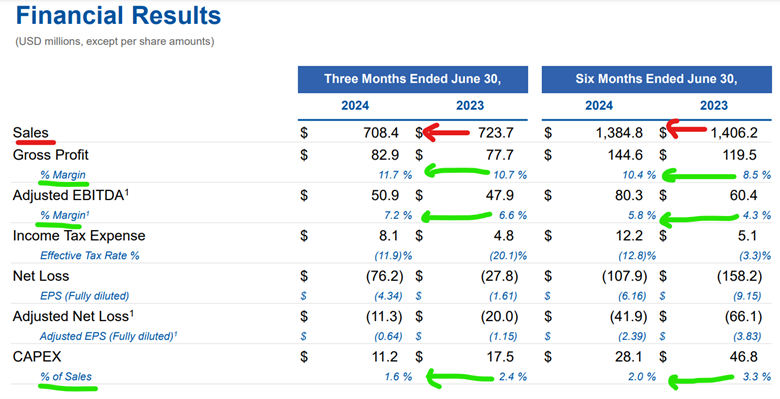

Cooper-Standard’s Q2 numbers looked average if you just read the headlines, but there was a lot to be optimistic about. Here’s the table investors will have seen:

Sales fell, but that was due to the divestiture of a rubber business; if that hadn’t happened sales would be up 1%, despite the general industry being down. Outpacing the market shows the company is taking market share, we like to see that.

Gross profit and EBITDA margins increased, while capex spend as a percent of sales decreased; the business improvements are working. What this means in the short term, is that CPS is getting closer to profitability and in the long term, should volumes increase, their operating leverage is even more acute. Good news from this table.

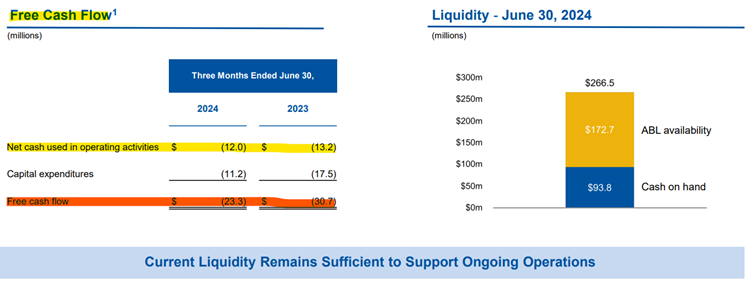

Another mediocre-looking table is the free cash flow table:

While they are less free cash flow negative than last year, they are still free cash flow negative. Like the disappointing sales number from above, there is a positive explanation for this:

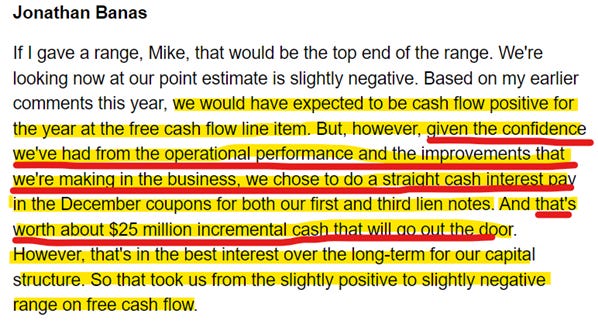

Because management saw business improvements, they were confident enough to elect to pay down debt, to the tune of $25M. If they had chosen not to, the company would be free cash flow positive, a big improvement from last year. I like management’s confidence and that they are prioritizing deleveraging. CEO Edwards confirms this in the call:

Another seemingly disappointing point in this earning report was the lowering of guidance. This always sounds bad but in this case the difference was miniscule and outside the company’s control. Sales and EBITDA guidance fell ~3%, reflecting a very mild softening in anticipated auto production. Here’s the updated guidance:

If you do the math, the company expects to be free cash flow negative, but again, that appears to be because they are electing to deleverage, otherwise the company would be free cash flow neutral to positive.

The only true disappointment of this quarter were the macro headwinds, highlighted by the CEO here:

To sum up his concerns, inflation is staying a little high, financing a new vehicle remains expensive, production volume is being revised down, the USD is weakening making it more expensive operate in other currencies, some OEMs are looking for price concessions, and dealer inventories are rising as people don’t want EVs as much as anticipated. While the company is turning around nicely, the industry isn’t yet, which will delay shareholders returns. I’m happy to wait, but if things to take a turn for the worse, I’d take a look at the facts and consider selling.

Overall, earnings looked disappointing, but were in fact largely positive. Macro was a headwind, but margins increased, market share increased, and default risk decreased. I’m a content shareholder.

What can we expect?

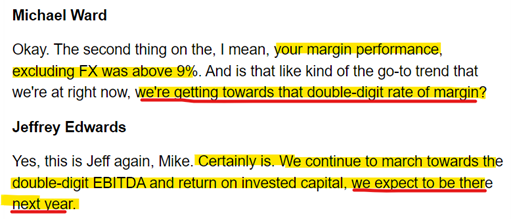

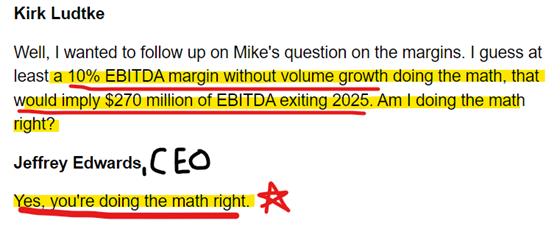

Management expects to reach 10% EBITDA margins in 2025:

This means, without production volume/sales increasing, the company could make $270M in EBITDA in 2025:

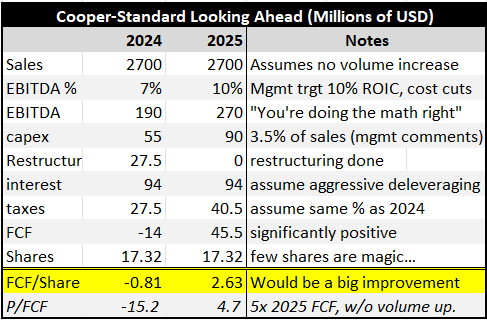

I took what information I could from the call and earnings report, and put it into a basic model:

Cooper-Standard is looking like a different company in 2025 if these assumptions end up being somewhat accurate. The big variable is production volume. Less volume and we’re looking at another tough year, same volume and the company is free cash flow positive, but more volume and we could see fireworks. Patience and keeping an eye on the macro will be key.

The CEO had alluded to this in the call:

He expanded on this in an interview with JP Morgan here, saying, “Going forward, clearly, volumes are going to start to pick up,” citing the normal stuff (age of the fleet being the biggest one) but also a leading indicator that was new to me: dealer incentives. If dealer incentives (like “employee pricing” for example) are going up, vehicles get cheaper and more people buy more autos, driving volume.

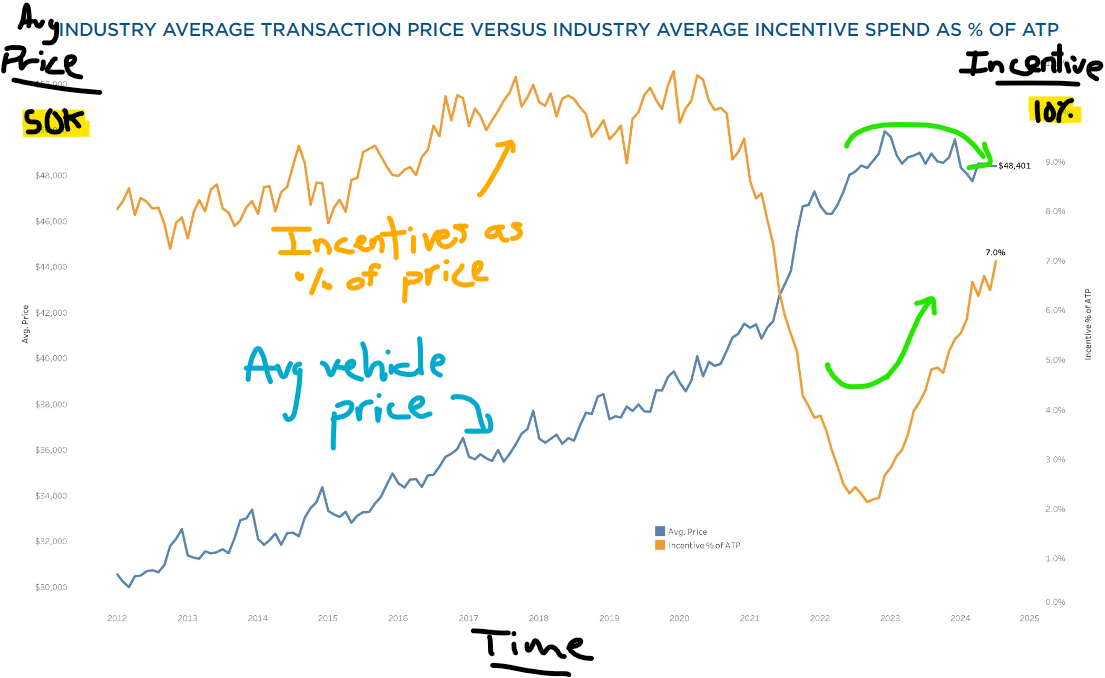

Here’s a graph of the trend he’s referring to:

We can see why he’s bullish on volume. Vehicle prices are rolling over while incentives are rapidly rising; vehicles are getting cheaper for consumers. How much cheaper? Let’s find out:

If new vehicle pricing and incentives revert to normalcy, new vehicles could get ~9% cheaper for consumers from todays prices, or around $4,000 per average vehicle. With the pandemic’s seller’s market still fresh in people’s minds, this emerging buyer’s market may appear particularly attractive to consumers, driving volume. Cheaper vehicles is a trend CPS investors like to see.

Vehicles are not necessarily getting more affordable, however. The remaining variable is financing. The analyst from Cox Automotive says:

Prohibitively high-rates are throttling new vehicle consumption, despite the fact those vehicles are getting cheaper on the lot. However, with the Fed due to cut rates in September, this last domino may start to fall.

That’s the bull case anyways. We shall see; this is all probabalistic.

Conclusion:

This trade’s success rests on three things:

Don’t go bankrupt

Enhance operating leverage

Wait for more auto production volume

In my view, all these things are progressing. Firstly, the company had its debt rating upgraded and is deleveraging, reducing default risk; secondly, margins are increasing despite lower sales, enabling greater operating leverage; and lastly, auto production volume is softening but not catastrophically so, while the average age of a US car is still over 13 years old, the number of drivers’ licenses continues to increase, prices are rolling over, incentives are normalizing, family-forming millennials are still the largest segment of the population, people still have jobs, retail sales are climbing, inflation has rolled over, and interest rates are coming down. Feel free to disagree.

I own the stock at a base of around $13 but have not added recently because it is already a large enough allocation for my risk-tolerance. I would likely sell if the US went into recession.

**I used a lot of Tom Hayes’ analysis but these views are all my own and don’t necessarily represent his.

NICE JOB!! I followed Hayes into this one too and I was too early as usual and timing is everything. You can buy a turnaround story but you need to buy it right.

The float is so small here too. Daily drip down is awful to watch. Such a controlled takedown. Who is selling?

I like your substack and think you make all the relevant points. A weaker USD should also help a great deal.

Cheers, Purple

Enjoyed reading.

Valuation wise why do you look at p/fcf? They are highly leveraged, doesn't it make more sense to value ev by (ebidta - maintenance capex) and then adjust to get equity valuation?