10 Unloved and Unorthodox Stock Ideas

Fish where the fish are

Introduction:

I haven’t been investing long enough to know at-a-glance what a market opportunity looks like, but this chart was helpful in figuring it out.

On a relative basis, small-caps, REITs, and treasury bills are as cheap as they have ever been in the last twenty years, while international equities are inexpensive enough to be interesting. Illustratively, volume on the TSX Venture Exchange, the home of small-caps, is 70% below the 15-year average (according to Donville-Kent’s latest note). Meanwhile, US Large cap, driven predominantly by the so-called “Magnificent Seven,” is as expensive as it has ever been. Some parts of the market are being overlooked.

Mean reversion is a powerful ally, so fishing in the small-cap, public real-estate, and international ponds, while avoiding the large-cap pond seems prudent.

Here are a few fish:

1) Canadian Net REIT – NET.UN

A small-cap and a REIT, NET.UN is a perfect example of what the market is overlooking right now. NET.UN is a Triple-Net REIT that owns grocery, C-store, and fast-food anchored retail properties outside urban areas, predominantly in Eastern Canada, Quebec in particular. The company has grown FFO/share and its distribution strongly in the past.

Rising interest rates have weighed on the shares, as the company has slightly more debt than would be comfortable on a lower quality business, but downside is likely priced in:

On all metrics, the stock is well below historical averages. Additionally, it currently yields 6.8% compared to a historical yield of around 4%. Giving me confidence is the fact insiders own 14% of the float, and management has been active buying back shares.

In short, the worst appears priced in, and should the worst not come to pass, investors will get shares in a growing business, valuation reversion, and a 7% distribution. I really like this one.

2) TerraVest Industries – TVK

Owns and acquires diversified, industrial businesses relating to home heating and cooling systems, compressed gas solutions, energy processing equipment and services. Many of their businesses operate in niche areas, meaning they face little competition and make good profits. Some areas are exposed to oil and gas cyclicality, but the company’s performance doesn’t depend on it, because they take their profits and redeploy them into acquiring more niche industrial businesses at low multiples and have been very successful doing so:

Very little of this 635% return was multiple expansion. For a company with such a record it trades at very low multiples on an absolute basis, leaving room for multiple expansion should investors take notice:

TVK has high insider ownership, buys back shares, and pays a 1.7% yielding dividend. Their debt is easily manageable. It also appears ready to benefit from but not require a commodity boom, should the supposed underinvestment in oil and gas turn out to be true.

In short, with TerraVest Industries, for 9x cash flow, investors get an established compounder, with aligned, proven management, operating in high-margin, niche markets with commodity upside. It’s hard to argue with this one.

3) RediShred Capital Corp. - KUT

RediShred is an industrial paper-shredding and recycling company. It’s viewed as a “melting ice cube” – meaning the core business should be slowing, paper after is all is going the way of the dodo. This turns out to be untrue, paper shredding revenues continue to grow at 10% for RediShred, as organizations continue to use paper, the law continues to require a lot of it be shredded, and RediShred takes and acquires market share. Additionally, much of their revenues are recurring, meaning KUT could be seen as a SaaS company, Shredding-as-a-Service.

The CEO owns shares and turned the business around 10 years ago. He reduces fixed expenses to expand operating leverage, strategically buys back shares, has reduced debt significantly, and makes acquisitions of franchisees and independent shredding companies at low multiples, further enhancing growth. Since 2019, the company has tripled EBITDA, but the price remains the same:

RediShred may see lower relative growth this year as recycled paper prices are lower than last year, but that is more than priced in. At just 7x EV/EBITDA, KUT hasn’t been this cheap since it was being turned around. There isn’t a great reason for the RediShred to be so lowly valued while the business performs better than it ever has. It’s a classic case of quality at a discount.

4) Currency Exchange International - CXI

Speaking of melting ice cubes, Currency Exchange International makes money by providing foreign currency to consumers, in airports for example, and institutions, like banks who need it for their customers and transactions. As such, this business is cyclical and correlates strongly with international travel. If that were the whole story, I wouldn’t be interested, but there are some unique aspects to CXI that make it more than just a banknote provider.

Here’s a quick list:

Their main North American competitor in airport exchanges, Travelex, left, leaving essentially just CXI in retail foreign exchange.

Have a schedule one Canadian banking license (like TD or RBC), and, after a strenuous due diligence process, have been approved to get USD notes directly from the Fed’s printing presses, reducing their costs significantly and providing credibility.

Have proprietary software and payments arm that facilitate international transactions, which have only come to scale recently, diversifying the business.

Are just beginning to expand their institutional (wholesale) banknote business internationally, expanding market opportunity immensely.

These developments have begun to transform the business and show up in the financials but not the valuation:

As we can see, EBITDA has picked up of late, while the price hasn’t fully matched it. If forward estimates are to be believed, CXI is currently trading at around 7x 2024 free cash flow. If the business is indeed better than it was, then this valuation won’t last long.

The CEO owns over 20% of the shares outstanding and is totally fanatical about and competent running the business. With no debt, it will be hard for it to go bankrupt. While CXI appears to be a melting ice cube with no moat, it has multiple avenues for growth and significant competitive advantages. A recession would be hard on this stock, but at 7x free cash flow, this appears priced in.

In short, Currency Exchange International emerged from Covid a stronger, more diverse, and growing business, but the market has yet to realize it.

5) Atlas Engineered Products (AEP) and 6) Fab-Form Industries (FBF)

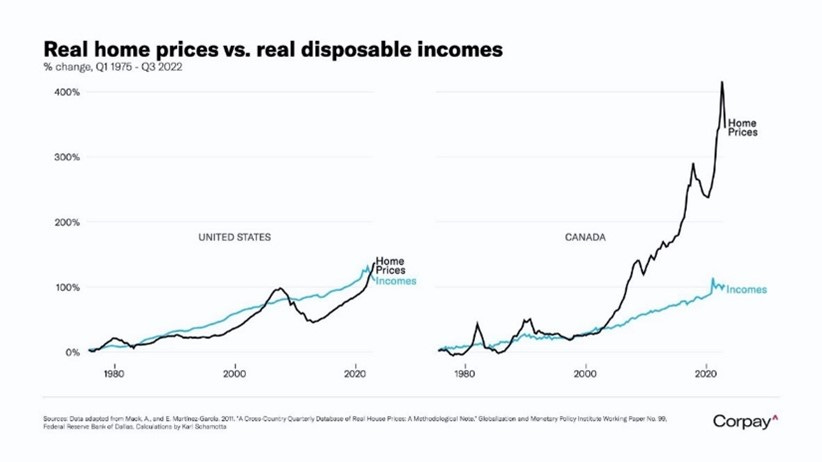

Typically, homebuilders would be seen as risky, but in Canada, we are so short of affordable places to live that there will be secular demand for housing for the foreseeable future.

AEP and FBF are going to be beneficiaries of the housing crisis in Canada because they both provide prefabricated home building, leading to quicker builds at reduced prices. AEP supplies primarily roof trusses, while FBF does insulated-concrete form (ICF) foundations. Both have a unique twist for investors. AEP acquires other truss plants with its cash flow and FBF innovates around ICFs, providing a foundation building system, with a growing and improving variety of proprietary products. Both have strong insider ownership, net cash balance sheets, and are profitably growing. I favour AEP right now, because it trades at a lower multiple, but FBF stays on my radar should it pull back.

In short, Canada doesn’t have enough houses, and Atlas Engineered Products and Fab-Form Industries provide quick, cost-effective ways of building them, with aligned, competent management leading the way. Cyclical though they may be these builders will prosper in the coming decade.

7) Fairfax India (FIH.U)

Fairfax India is a subsidiary of Prem Watsa’s Fairfax Financial (FFH) and acts as an investment vehicle and holding company for many of the company’s Indian investments. It has a variety of assets, but by far its most valuable is a 59% stake in India’s third largest airport (in Bangalore, the supposed “Silicon Valley of India”). The airport is irreplaceable and regulated to provide a high teens return, as long as traffic predictions are accurate. Thus far, actual traffic has exceeded expectations, implying the airport may be undervalued.

Here’s what they own and how it’s being valued:

A few things to note. First, many of its businesses earn in rupees and are valued in them, but the company reports in USD. A weakening USD would provide a tailwind to earnings and valuations as the rupee is worth more in relation. Second, most of the assets are plays on the economy doing well. Some of them look great, like the National Stock Exchange while others look very cyclical, like the chemical company. Lastly, it can be hard to trust the valuations of privately-owned companies, but at the current price, investors are nearly getting them for free, as 94% of the stock’s price is made up of just the airport and its public investments.

A cogent argument can be made this doesn’t deserve to trade at book value, as most holdcos don’t and this one has a fairly high fee structure. The company takes 1.5% of book value and 20% of any growth above a 5% hurdle rate (meaning if the company grows book value at 10% annually, they charge 2.5%). I really don’t love this, but when I think about it, access to and expertise in India’s private markets is probably worth it. How else would I be able to buy an Indian airport?

Historically the company has grown book value at a fair clip and its valuation has reflected that, but recently its valuation has not kept up:

In short, though the fees do rankle, Fairfax India creates value where I can’t, owns an irreplaceable asset at a good price, and is historically undervalued.

8) Ceapro (CZO) and 9) Cipher Pharmaceuticals (CPH)

Ceapro and Cipher are interesting healthcare/pharma/biotech plays. Both are being valued based on their legacy businesses. In the case of Ceapro, they provide patented oat-based derivates for brands like Neutrogena and Aveeno, while Cipher’s main product is a widely prescribed ACNE treatment. Both are strongly cash flow positive and with net cash balance sheets. Ceapro is growing (though it’s taken a temporary break) while Cipher is maintaining revenues. One could make the argument that these companies are undervalued just based on their legacy operations, but the market doesn’t seem to agree. I might not mention these companies myself if it weren’t for the value hidden beneath the surface.

Ceapro has a patented technology platform (“PGX”) that can be used to get and enrich plant compounds and is currently unique. They focus on oats, but the platform could be used for anything, from cacao to green tea, to cannabis. Management plans to reinvest cash flow into pursuing new plant compounds for medicinal, nutritional, and cosmetic uses. It’s hard to say as an outsider how well their pipeline is doing but the platform could result in significant value over the long term.

Cipher has the Canadian rights to a promising, late-stage nail fungus treatment. The treatment was just approved in Europe, where pharma giant Bayer owns the rights. The current nail fungus treatment is daily, oral, and has side effects. This new treatment is once a week, topical, and with only cosmetic side effects (the nail goes white until it grows out). This side effect is the main reason it hasn’t been approved in North America yet, but a new trial has been initiated, with the plan to generate revenues in North America by 2025. Canadian sales of the drug are estimated to nearly double Cipher’s revenue.

Neither of these healthcare/pharma/biotech companies are guaranteed homeruns, but they also aren’t going to zero because they have strong legacy businesses piling up the cash. Their valuations are very undemanding, CZO trades at 8x EV/EBITDA while CPH trades at just 3x EV/EBITDA.

In short, with undemanding valuations, cash flowing legacy businesses, and drug-related upside with catalysts, Ceapro and Cipher present a great risk reward.

10) Cooper-Standard – CPS

Not for the faint of heart, Cooper-Standard is an original auto-parts manufacturer for Ford, General-Motors, and many others, that nearly went bankrupt during covid. It has a lot of debt and is relying on a return to profitability and huge operating leverage (meaning their costs are largely fixed, so any increase in revenues past a certain point goes directly to the bottom line) to pay it back. The debt is serviceable short-term (they were free cash flow positive in the latest quarter), and not a problem should new vehicle demand return to pre-covid levels.

The chip shortage slowed new car production leaving unmet demand, and interest rates making the cost of buying a used car quite high, will lead consumers to buying new vehicles, benefitting CPS. Should mean reversion occur, car production will return to pre-covid levels, and CPS should earn per share what it did in 2019, around $7/share:

At the current price of around $14, CPS could be seen as trading at 2x Forward P/E. At peak multiple, CPS traded at 20x earnings and at a trough, 10x. Either way, at $70 or $140/share, that’s a lot more than the current $14. I’m watching company guidance and vehicle production numbers closely, both of which are currently beating expectations.

In short, if a calamity happens, then Cooper-Standard could go to zero, but should the far more likely event occur and things go back to normal, investors could see a 5-20x multi-bagger. In this case, I consider the risk to balance the reward, but not so much as to make it a huge position. I thought it was worth mentioning though.

Conclusion:

The stock market is a lot more than the Magnificent Seven or the S&P 500. The companies I just highlighted are ten that are not getting attention – yet. As the last pockets of value in the large-cap space get consumed, and risk comes back into the market, companies like the ten I just highlighted will likely get some love.

Not all are going to work out, and the information here is not enough to make an investment decision, so please do your own due diligence. I got these ideas from screens, blogs, twitter, and podcasts, then did my own due diligence.

I own all of them except for Cipher Pharmaceuticals but am thinking about buying it.

Thanks for reading!